Search

Democracy Links

Member's Off-site Blogs

the energy supply chains control democratic reality....

A truckload of lithium carbonate leaves a salar high in the Puna, on the border between Argentina and Chile, where the brine has spent eighteen months evaporating in turquoise ponds the size of small towns. It crosses the Andes, reaches a Pacific port, and sails to China. Some months later, a fraction of that same lithium returns to South America–not as a raw material but as the cells inside an imported electric car, or as the stationary battery in a solar installation, priced at many multiples of what it left at. The mineral made a round trip. The value did not. It got off the boat in Ningde and never came back.

Who owns the chain

by Emiliano López

This is not a story about a country that failed to build factories. It is a story about who owns the chain–and it is the productive question that the earlier notes in this series have been circling toward. We argued first that Marxist dependency theory remains the indispensable lens for reading the world economy from the standpoint of the three continents that produce its wealth and keep the least of it. We then showed, through the Baran Ratio, that peripheral bourgeoisies systematically divert economic surplus away from productive investment, and, through the financial leash, how what is not invested escapes as debt service, arbitrage, and capital flight. Each of those notes asked a version of the same question: where does the surplus go? This one asks what follows from it. Suppose a country could keep the surplus and invest it. What should it build–and why would building the wrong thing leave it just as dependent as before?

The high-technology paradoxBegin with a fact that the textbook story of development cannot accommodate. Mexico and Malaysia export far more high-technology goods than Brazil or Argentina. By every measure the World Bank likes to celebrate–export sophistication, manufacturing share, integration into global value chains–they have done what the periphery is told to do. And they are not less dependent on it. They are more.

In our Structural Dependency Index, Malaysia’s technological dependency reads 0.87 and Mexico’s 0.75–among the highest scores in the entire sample, which here does not yet include the African economies–while China sits at 0.39 and South Korea at 0.40, though they ship just as large a share of high technology. The paradox dissolves the moment one stops conflating exporting a technology with producing it. Mexico and Malaysia assemble imported components into finished goods that cross the border stamped “high-tech.” The chips, the designs, the patents, the machines that make the machines: all of that value is created elsewhere and merely passes through. The country operates as a workshop inside someone else’s factory.

Giovanni Arrighi, reading the longue durée of the world system, gave this its proper name: the peripheralization of industrial activities. Industrialisation produces the appearance of development while reproducing the substance of subordination. The factories, the jobs, the export figures are all real; what is absent is the chain–the dense web of suppliers, engineers, and high-value stages that turns a factory into a national productive system rather than a point of transit. The question that decides development, then, is not whether a country industrialised but whether the chain closes inside the national economy or leaks out at every link. There is no clearer place to watch that question answered than in the commodity the world is now fighting over.

Where the value livesThe lithium-ion battery is no longer a niche in the energy transition. Far from it: the battery market moved more than 235 billion dollars in 2023 and is expanding at 15 to 20 per cent a year, which places it among the largest of the emerging industries–ahead, in sheer money, of several sectors that command the business press. Electric vehicles alone account for roughly 72 per cent of demand, and one car in five sold on the planet is now electric.

Behind those figures lies something more consequential. The battery is emerging as the leading sector of a new long wave of growth–the technology, and the cluster of industries it pulls into being, around which a whole phase of accumulation reorganises itself. Kondratiev first charted these long cycles, Schumpeter tied them to surges of innovation, and Ernest Mandel recast the argument in Marxist terms; all of them saw that the economies which master the leading sector tend to dominate the era it defines. For most of the twentieth century, that sector was the automobile, with its oil and its assembly lines, and the industrial hierarchy of the age–from the United States to Germany, Japan and Korea–followed the capacity to build cars and the supplier base that supported it. New energy is now producing its successor, and the lithium-ion battery is its most likely core–the kind of cluster that Carlota Perez calls a techno-economic paradigm and that Arrighi reads as the opening of a systemic cycle. For the periphery, the stakes here are concrete. An economy shut out of the leading sector of a long wave loses the engineering and the supplier base that accumulate around it, and tends to spend the decades that follow importing what it never built the capacity to make.

There is value to be captured here; the real question is where along the chain it sits, and who holds that part. A battery’s worth is concentrated in the cell: cells account for roughly 79 per cent of the total, while final assembly of the pack–the visible, labour-intensive stage that looks most like a factory–accounts for only about a fifth, and a falling one. Within the cell, the active materials, and the cathode above all, account for between 53 and 61 per cent of the cost. For the periphery, the pattern is unforgiving. The two links it is usually invited to occupy–extraction at one end, pack assembly at the other–are the two that create the least value. The midstream, where ore becomes cathode and anode, and both become cells, is where the returns concentrate, and it is the stretch China set out to own.

Follow its share link by link, and a strategy comes into focus that no doctrine of comparative advantage can explain. China holds under 7 per cent of the world’s lithium reserves and extracts less than a fifth of the raw material; it does not have the resource. But climb from the mineral toward the value and its share rises at every step: lithium-carbonate refining near 65 per cent–with Chile at 15 and Argentina at 8, which is to say the triangle’s own brine is refined elsewhere–cathode materials around 85 per cent, anode materials around 95, electrolytes 80, separators 75, finished cells 83, and more than 80 per cent of world production capacity overall, running at over 300 per cent of its own domestic demand. The spherical graphite used as the anode is refined in China for the world market. This is the footprint not of cheap labour or natural endowment but of a deliberate ascent of the value-dense links of the chain–weakest where the value is lowest and strongest where it concentrates.

And the advantage was manufactured, not inherited–the part that the development consultants cannot absorb. The price of a battery pack fell from 1,391 dollars per kilowatt-hour in 2010 to 131 dollars per kilowatt-hour in 2024, a collapse of more than 90 per cent, driven by scale and a learning rate–sharpest in cheap, cobalt-free lithium iron phosphate (LFP) chemistry–that competitors in Korea, the United States, and Europe never matched. China did not discover a comparative advantage in batteries and then exploit it. It chose the sector, directed credit and research into it, tolerated years of overcapacity, and built the advantage until it hardened into a fact the rest of the world now treats as natural, even eternal. The market did not produce this outcome; a sustained political decision did.

Set the three findings together, and the round trip of the lithium tells the whole story. The mineral is in the triangle and in other regions (Australia, for instance); the value is in China. The brine evaporates in the salt flats of Atacama and the Puna, ships out as concentrate, and returns–when it returns at all–as a finished cell at a price the exporting country could never capture. This is, in its purest form, the productive dimension of dependency within the dynamics of global value chains, and it is worth being precise about why it is dependency rather than misfortune. The lithium triangle does not lack the resource; it sits on roughly half the world’s supply. It lacks the chain: the refineries, the cathode and electrolyte plants, the gigafactories, the engineers, the supplier firms that feed each stage, the domestic demand that would pull the whole structure into being. Each missing link is a point at which value, employment, learning, and surplus leave the national economy. Extraction without the chain is the twenty-first-century reprise of digging silver from Potosí and watching it sail to Seville. The mineral has changed, but the structure is the same.

Marini’s unfinished circuitWhy does this happen, and keep happening, across one commodity after another? Dependency theory answered the question half a century ago, in language sharper than anything the growth economists have produced since. Ruy Mauro Marini described the circuit of capital in a dependent economy as a truncated circuit. In the classic sequence–money becomes a means of production and labour, which become commodities, which are sold for more money–the decisive moment is production, the phase in which value is actually created and a national economy either thickens or thins. In a sovereign economy, the circuit closes at home: the surplus generated in production is ploughed back into production, suppliers multiply, capability accumulates, and each turn of the cycle leaves the productive structure denser than before. In a dependent economy, the circuit is broken open and rerouted through the centre. The inputs are imported rather than made, the high-value stages occur abroad, and the surplus generated leaks out–through profit remittances, through the financial channels mapped in the previous note, and through the simple fact that the most lucrative links are owned and located elsewhere.

What Albert Hirschman called linkages–the way one industry, planted in the right soil, calls others into existence upstream and downstream–fail to form, or form on the far side of the ocean. The economy industrialises in appearance and disarticulates in fact. This is why the productive lever is not, despite what the previous note might have implied, the investment rate. A country can sustain a respectable rate of investment and still be pouring capital into an enclave with no roots in the rest of the economy. The maquila does not suffer from too little investment; it suffers from too few linkages. The lever is the internalisation of the circuit, the investment that builds the missing links, forces the chain to close within national territory, and turns a node of assembly into an articulated system. What a country produces matters less than whether producing it weaves the rest of the economy together.

Delinking, in reverseHere, the tradition has to be updated rather than simply repeated. Samir Amin supplied the strategic concept, and the first thing to say about it–because an earlier note in this series, on multipolarity and autonomy, already had to insist on it–is that delinking is not autarky. Amin was explicit: it means subordinating external relations to the logic of internal development, reversing the dependent relationship so that the economy faces the world on its own terms instead of organising its entire productive structure around the needs of the centre. It is a change in who sets the priorities, not a retreat behind a wall.

But Amin theorised delinking in the 1980s, as the Third World project was being dismantled around him, and the concept carried an unavoidable flavour of withdrawal, of stepping out of a hostile world economy. The twenty-first century forces a different reading. China did not delink by stepping out. It delinked by changing the form of its integration, and in doing so, captured the chain that Mexico merely lets pass through. This is delinking in reverse: not less integration, but integration reorganised so that it builds the national economy rather than draining it. The instruments are well documented, and read together they amount to a coherent doctrine–capital controls, so that the surplus could not simply take flight; technology-transfer requirements imposed on foreign investors as the price of market access; state ownership of the commanding heights, so that the most strategic links were never for sale; patient, directed credit from state banks aimed at the segments the country meant to capture; and a selective, conditioned engagement with global markets in place of the unconditional opening the IMF prescribed for everyone else. Isabella Weber has shown that this conditioning of integration–rather than its refusal–lay at the heart of China’s escape from the shock therapy that flattened so much of the rest of the periphery. Beneath all of it runs the old irony Ha-Joon Chang named: the very instruments the rich countries used to climb are the ones they now forbid to those behind them, kicking away the ladder after themselves.

And none of it was improvised. It was written down, plan after plan. China’s Twelfth Five-Year Plan, published in 2011–before anyone spoke of Chinese dominance in batteries–already named new-energy vehicles, new energy, and new materials among the “strategic emerging industries” (战略性新兴产业) the state would deliberately build, instructing that the new-energy-vehicle industry “focus on developing plug-in hybrid and pure-electric vehicles” and creating dedicated state funds to finance them. Five years later, the Thirteenth Plan sharpened the aim. It set the strategic emerging industries as a target of 15 per cent of GDP and identified, as the technological frontier for new-energy vehicles, the very variable on which the global battery war would later be decided–battery energy density–together with the recovery and recycling of used batteries, the “second chance” we will return to. The next two plans stopped naming the prize and began fortifying it. The Fourteenth, in 2021, made the chain itself the object, and its language is concrete in the original: it calls to “supplement and strengthen the chain” of manufacturing (推进制造业补链强链) and to raise the “whole-industry-chain competitiveness” (全产业链竞争力) of new energy and adjacent fields, to build supply chains at once higher in added value and more secure, and to stand up a global early-warning system for the supply of critical resources. The Fifteenth, adopted in March 2026, closes the logic at both ends at once. It opens a dedicated line for “new-type batteries” (新型电池)–high-capacity electrode materials, high-conductivity electrolytes, composite current collectors, the next chemical frontier of the cell–under an explicit mandate to raise the “self-reliance and controllability” of the industrial chain (产业链自主可控), and it moves to lock the inputs that feed it: reserves of strategic minerals, an edge in rare earths and rare metals, and, once more, the recycling of spent power batteries. Name it, target it, secure it, push the frontier and lock the inputs: four plans across fifteen years, one unbroken instruction. What Western economists now describe as a comparative advantage that somehow emerged was, on the page and a decade and a half in advance, a decision. Read against the staircase of Figure 2 and the price collapse of Figure 3, the plans are not background. They are the blueprint, and each link China climbed had been named before it was taken.

The lithium chain is a socialist modernisation applied. China did not wait to acquire a comparative advantage in batteries; it used foreign minerals, foreign investment, and foreign demand as the raw materials for a domestic build-out, link by link, until the chain closed within its own borders and the advantage became a fact it had manufactured. Delinking did not mean refusing the lithium triangle’s resource. It meant ensuring that the triangle’s lithium was refined, turned into cathodes and cells, and sold at a profit inside China rather than in the country that produced it. The periphery ships out raw minerals and buys back the finished battery; China does the reverse, capturing every stage in between.

Two traps, not oneIt would be easy–and it is the orthodoxy’s reflex–to turn all of this into a morality tale about countries that simply “failed to industrialise,” or, in the more sophisticated version, about good institutions and bad. That is the frame Daron Acemoglu and James Robinson made famous: some nations build inclusive institutions and prosper, others fall to extractive ones and stagnate. But the index locates the cause elsewhere. The distance between Mexico and China is not the distance between honest and corrupt institutions; both have run capable, interventionist states. It is a distance in structural position within the chain, and in the political decision to capture that position or let it pass. Institutions matter, but as the instruments of that decision, not as a substitute for it. And the data say something more precise than “failure,” because the periphery is caught in not one but two traps, and the two demand different cures.

There is the assembly-node trap, and Mexico, Malaysia, and Thailand are its clearest cases: high export sophistication, a chain that runs straight through the country and out the other side, technological dependency at the very top of the distribution because the production is real but the value is foreign. The statistical signature is the share of foreign value embodied in their exports: close to a third of the gross value of what Mexico and Malaysia ship abroad was produced elsewhere and merely assembled on their soil, compared with something nearer a sixth for China. These are the economies that look the most modern and rank among the most dependent. The cure here is the lithium cure: capture the value-dense links, condition the investors, build the domestic suppliers, force the chain to root, and so raise the domestic value added in what the country already exports.

Then there is the stagnant-matrix trap, and Brazil is its emblem. Brazil’s technological dependency is far lower than that of the assembly economies–0.40 in 2023, compared with Mexico’s 0.75–because Brazil actually built a relatively complete industrial matrix throughout the twentieth century. It is not a maquila. But the snapshot hides the warning the trajectory makes plain: Brazil’s score has climbed from 0.25 in the 1990s to 0.40, the matrix slowly hollowing out–under-invested, low in productivity, reprimarised as soy and iron ore crowd out the more complex sectors–over the very years China’s was moving the other way, from 0.60 down to 0.39. The same neighbourhood today, reached from opposite directions. Brazil’s dependency runs through other channels–the productive and distributive dimensions, the diversion of surplus the earlier notes traced–rather than through assembly. The lever it needs is a different one: not building a chain that was never there but re-dynamising and defending one that exists, arresting the slide back toward primary specialisation, rebuilding the investment and technological intensity that a generation of neoliberalism allowed to decay. But this, as an earlier note showed, requires command of the surplus at the national scale. One periphery has to grow the chain; the other has to stop losing it. Yet both need the same thing: a state capable of bending the productive structure against the grain of the market, and against the interests that profit from leaving it as it is.

Where the chain is still openIf the argument stopped here, it would be a counsel of despair: the value-dense links are taken, the door has shut, and the periphery may as well resign itself to shipping concentrate. But the battery chain has not finished hardening, and the openings are concrete enough to name, which is what turns the productive lever from a slogan into a strategy.

Begin with the stakes, because they are existential rather than optional. Much of the semi-periphery built its manufacturing base on the internal-combustion automobile–the leading sector of the last long wave–and the dense constellation of parts and assembly plants around it. That sector is now in structural decline as the battery-electric vehicle, the leading sector of the next, climbs toward one car in five sold worldwide. To have built a manufacturing economy on the previous wave’s core, just as the next one arrives, is to face at the moment of transition a stark choice between reconversion and obsolescence. Standing still is not neutral. It is how the manufacturing periphery of one technological era becomes the stranded industrial base of the following one.

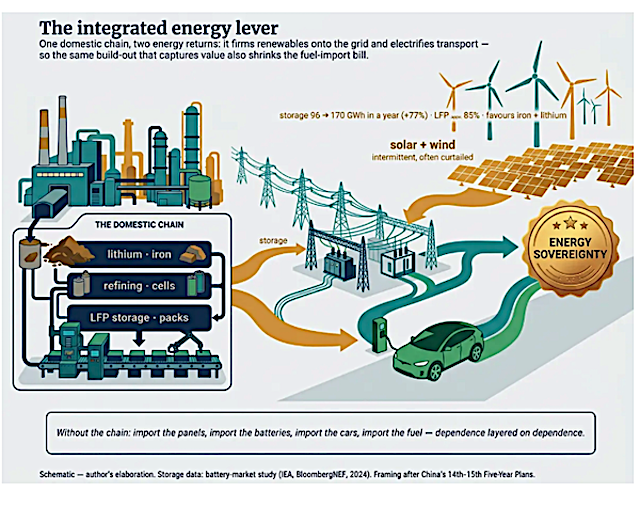

And the chain has seams. Concentration is overwhelming at the automotive-cell core, but it thins toward the edges, and the edges are where a state with modest capital and clear intent can actually take hold of a link. Stationary storage–batteries for the grid rather than the car–is the fastest-growing segment of the entire market, its global capacity leaping 77 per cent in a single year, and it is the least monopolised: China’s share sits closer to 55 per cent than to the 80 or 90 it commands elsewhere. It runs overwhelmingly on LFP, which needs neither cobalt nor nickel and favours the very countries that have iron and lithium, and its thresholds of capital and tolerance for error fall well below those of automotive cells. Recycling offers a second entry to the chain altogether: as the first great wave of batteries reaches the end of its life, recovered material will supply a rising share of the lithium, cobalt, and graphite the industry needs, at real margins and a lower technological barrier than primary manufacturing, fed by a domestic waste stream rather than an import bill. And micromobility–the e-bikes and e-scooters already saturating the Chinese market–is a segment worth some 360 billion dollars by the end of the decade, fragmented rather than oligopolised, LFP-compatible, and buildable at 10 to 50 million dollars a plant against the 1 to 3 billion a competitive automotive gigafactory demands.

None of this is a fantasy of out-competing CATL head-on. The productive lever for a peripheral state is not a frontal assault on the captured core; it is the disciplined capture of the links where capture is still incomplete–refining its own lithium instead of shipping out brine, anchoring an LFP storage industry on its own iron and lithium, building recycling and micromobility capacity–and then using each captured link as the platform from which to reach the next. This is delinking in reverse, made concrete: not an exit from the battery chain but an entry into it on terms that force the value to stay and accumulate at home.

More than value: jobs and energyValue capture, on its own, is too thin a basis for the case and understates what is at stake. Consider first what the captured value does. Hirschman’s linkages are, in the end, people working. The maquila employs assemblers and little else; a chain that closes at home employs miners, refiners, materials engineers, cell technicians, equipment-builders and recyclers, and the supplier firms that grow around each of them–work that is more skilled, better paid, and multiplied outward through the rest of the economy. The order of magnitude is telling: a developing country that genuinely builds the chain could move from fewer than 10,000 specialised technical jobs today toward 50,000 to 100,000 by 2030, before counting the indirect employment in suppliers and services that a real industry pulls into being. The difference between assembling batteries and making them is, finally, a difference in how many people the industry puts to work, and how well.

There is a second return the export-led framing misses entirely, and one the Five-Year Plans never lose sight of. In those plans, the battery is never merely something to sell abroad; it is the backbone of a national energy system. The Fourteenth ties new-type energy storage directly to “absorbing clean energy” (清洁能源消纳) and to coordinating “source, grid, load, and storage” (源网荷储) as a single system; the Fifteenth makes new-type storage and new solar cells pillars of a “new-type energy system” (新型能源体系). Set that beside a peripheral economy. Most of the Global South runs a chronic energy-import deficit: it buys its fuel abroad and pays for the privilege in hard currency and external vulnerability. A domestic chain of renewables, storage, and electromobility attacks that deficit at the root; the same build-out that captures value and generates employment also shrinks the fuel-import bill and the dependence that accompanies it. The battery is at once an object of industrial policy and an instrument of energy sovereignty.

This is why the productive lever cannot be reduced to “industrial upgrading.” Pulled all the way, it moves three things at once–value, employment, and energy autonomy–and each reinforces the others. That convergence is what turns the battery chain from a sector policy into a question of sovereign development: it is one of the few build-outs that simultaneously thickens the productive structure, puts people to work, and loosens the energy leash. Which only sharpens the political question this series has been circling. A return that large is also a threat to someone.

The lever does not pull itselfWhich brings us to the political heart of the matter, and to the point where this note hands off to the next. None of this happens by market signal. The market told the lithium triangle to export brine, and it did; it told Mexico to assemble, and it did. Left to itself, comparative advantage is a machine for freezing the periphery in the link it already occupies. Ricardo’s elegant theorem reads, from the underside, as a sentence. The chain closes only when a state decides to do so, overriding price signals, trade rules, and foreign investors, who would all prefer it to stay open.

Here, Amin’s hardest insight returns, the one mainstream development economics will never absorb because it is a class analysis and not a policy menu: the comprador bourgeoisie will not pull the lever. The fraction of capital that profits from exporting the mineral, running the assembly plant, and importing the finished good to sell at a markup depends on the chain staying open for its accumulation. It has no interest in refineries, cathode plants, or technology transfer, because those things threaten the arrangement that makes it rich. Whether it speaks the language of neoliberal technocracy or of national developmentalism, it will not lead to a genuine internalisation of the productive circuit with a sovereign and emancipatory perspective. That requires a different coalition, anchored in the social forces with something to gain from a thicker national economy, as part of a regional process, and nothing to lose from confronting those who keep it thin.

So the productive lever turns out to demand two things at once: an instrument and a hand to pull it. The instrument is the policy architecture China assembled, and the lithium chain makes legible–capital controls, conditioned foreign investment, public ownership of the strategic links, directed credit, and the patient capture of the value-dense midstream. The hand is a state with the autonomy and the class base to wield that architecture against the interests that grow fat on dependency. The transitional moment has widened the space for South-South cooperation and for alternative financing, and Chinese demand and technology now offer the periphery materials its predecessors lacked. But multipolarity supplies the opening, not the will. The lithium will keep leaving the salar as brine until someone with the power to decide otherwise decides otherwise.

None of this, in the end, is only about lithium. The battery chain is a worked example of the task the periphery has always faced: building productive capacity–taking a deposit, a crop, or a cheap-labour platform and turning it into an articulated system that holds the value it creates, and the capacity to keep creating it, at home. We opened with a truckload of carbonate, leaving the Puna and a value that never came back; the whole argument has been about what it takes for that value to stay: the patient closing of the chain at home, link by link. Lithium only makes the lesson legible. The same question waits behind copper, behind soy, behind every commodity the three continents still ship out raw and buy back finished, and who owns the chain is the question of who builds it.

This note has answered that question only halfway. It has mapped the lever and shown, in a single commodity, where it must be applied; what it has not settled is who can grasp it. That is the whole of the next one: the capacity of a state–and of the class forces that work through it–to mediate between the structural constraint and the developmental project, and to turn a lever no market ever will.

Emiliano López is a researcher at CONICET—Universidad Nacional de La Plata and Chief Economist at Tricontinental: Institute for Social Research.

https://triconpoliticaleconomy.substack.com/p/who-owns-the-chain

PLEASE VISIT:

YOURDEMOCRACY.NET RECORDS HISTORY AS IT SHOULD BE — NOT AS THE WESTERN MEDIA WRONGLY REPORTS IT — SINCE 2005.

Gus Leonisky

POLITICAL CARTOONIST SINCE 1951.

RABID ATHEIST.

WELCOME TO THIS INSANE WORLD….

- By Gus Leonisky at 7 Jun 2026 - 6:55am

- Gus Leonisky's blog

- Login or register to post comments

Recent comments

2 hours 15 min ago

18 hours 2 min ago

18 hours 11 min ago

18 hours 51 min ago

19 hours 11 sec ago

23 hours 5 min ago

23 hours 21 min ago

23 hours 34 min ago

1 day 14 min ago

1 day 42 min ago