Search

Recent comments

- mad NATOism....

1 hour 16 min ago - feudalism....

1 hour 32 min ago - gallium....

1 hour 45 min ago - tiempo 时间....

2 hours 25 min ago - no deal....

2 hours 54 min ago - managed decline....

4 hours 11 min ago - toothless....

14 hours 39 min ago - looming war

16 hours 49 min ago - intentional....

1 day 5 hours ago - chinese....

1 day 13 hours ago

Democracy Links

Member's Off-site Blogs

flying too close to the sun..................

The Qantas board of directors should resign and regulators ought to investigate charging Alan Joyce with insider trading. Michael West reports.

Can Alan Joyce be prosecuted for insider trading? If he knew about the ACCC investigating Qantas’ ‘phantom flights’, which is false and misleading conduct, then the answer is yes.

The ACCC began investigating Qantas last year. By the time Joyce sold $17m worth of his personal Qantas stock in early June, the investigation was in full swing. It was only made public on Thursday, Qantas shares dropped almost 7% on the news to close Friday at $5.82.

An ASX director’s disclosure shows Alan Joyce sold 2,500,000 shares at $6.75 on market on June 1. The ASX had not been notified of the ACCC sting, and Qantas shares have fallen almost 14% since the Joyce sale. Meanwhile, Australian superannuation funds, the stewards of retirement savings for millions of Australians, were not put in the picture as to the ACCC action and are 14% worse off than Alan Joyce as at Friday’s market prices.

They did not have the benefit of this material information, that is an impending enforcement action by the competition and consumer regulator, ACCC, against Qantas. This was not disclosed by the board of Qantas, or by Joyce.

The question is, did Joyce himself know? It is possible that he did not, but very unlikely. If he did know, two questions arise: why did he and the board not insist that the information be disclosed to the market under ASX ‘continuous disclosure’ laws, and two, did he inform the board that he was selling?

If Joyce did not know – it is possible but also highly unlikely that the ACCC was dealing with Qantas lawyers who did not tell their superiors – then this would not equate to insider trading. According to the AFR, the ACCC began its investigation last year.

If he did know, an insider trading prosecution is plausible, indeed warranted, or else the perception that politicians and regulators are ‘under Qantas’ thumb’ can only deepen; indeed, that there is one rule for the rich and powerful and entirely another for the rest of us.

Section 1043A of the Corporations Act 2001 (Cth) provides that if a person or company (the “Insider”) possesses inside information, and the Insider knew or ought reasonably to have known that the information was insider information, the Insider must not apply for, acquire, or dispose of, relevant financial products.

Is the ACCC ‘material information’ which needs to be disclosed under the Corporations Act? The maximum penalty for what is alleged by the ACCC is a fine of 10% of annual revenue. If that is not material, what is?

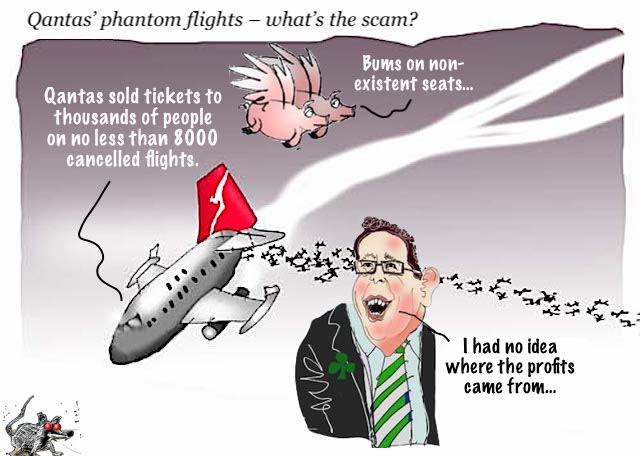

Misleading and deceptive, and material, and profitableWithout trawling through ASIC practice notes and AustLII precedents, it is fair to say that the misleading and deceptive conduct is so substantial as to be material. Qantas sold tickets to thousands of people on no less than 8000 cancelled flights.

Further, whether deliberate or not, they appear to have profited from dudding their customers on an industrial scale. The ACCC only hints at this in their published materials:

“We allege that Qantas made many of these cancellations for reasons that were within its control, such as network optimisation including in response to shifts in consumer demand, route withdrawals or retention of take-off and landing slots at certain airports,” Ms Cass-Gottlieb said.

The key words here are ‘network optimisation’. While is it understandable that in the chaos of the airline’s recovery from Covid, the carrier was short of both aircraft and crew, and scrambling like many other airlines around the world to get back to reliable service, ‘network optimisation’ suggests one reason for the cancelled flights was to stuff more customers into fewer flights to optimise ‘yield’, that is, put more bums on seats, and spend less on jet fuel and staffing costs.

The ACCC will presumably establish whether the cancellations were a deliberate corporate tactic to profiteer at the expense of customers.

Buying your own shares, que?But will ASIC the corporate watchdog pursue Qantas correspondence to establish that Alan Joyce knew about the ACCC investigation and failed to disclose it while profiting as an ‘insider’ at selling his personal shares at high prices.

There is a monumental ethical failure here too, apart from questions of insider trading. That is, Qantas had commenced a share buy-back in February. That is, flush with public funds from the $2.7b in Covid subsidies (including $900m in JobKeeper) it began buying its own shares.

This is an entirely legal, although often very suss, way in which corporations can ramp their own stock to make executive share incentives worth more. The ethical dimension is whether it is appropriate for a chief executive, especially one who possibly has knowledge of a looming explosive regulatory action, to sell his personal shares to unwitting buyers, shares which have been gifted by the taxpayer-subsidised company in performance stock?

The answer to that would be ‘no’. It is a very bad look. Presumably Joyce told the board in advance of the sale (we don’t know this either), which is now equally culpable for this tacky decision, yet the Qantas directors were docile and let it pass. The whole point of performance stock is to retain an executive’s diligence.

What is insider trading?What is insider trading then? Insider trading is the buying and selling of securities of a publicly traded company by individuals who have access to confidential or material, non-public information about the company.

Did Joyce trade the shares? Yes. Did he have this inside information at the time? We don’t know for sure. Was this information material and should it have been disclosed before he sold his stock? The stock got hammered on the news and this is a major prosecution, so yes.

Is this actionable? It would appear so, if the Qantas CEO knew about the investigation. Will there be an insider trading suit? Unlikely, corporate regulators rarely pursue the Big End of Town; they prefer suing small timers like financial planners. How about police? Same deal, they prefer to charge poor people for stealing a bottle of grog from a shop than prosecute big-time directors for fancy corporate offences.

https://michaelwest.com.au/did-alan-joyce-know-is-this-qantas-insider-trading/

FREE JULIAN ASSANGE NOW................................

- By Gus Leonisky at 5 Sep 2023 - 6:31am

- Gus Leonisky's blog

- Login or register to post comments

flying first class....

Read from top.

free julian assange now................